Spreads

Spreads

Spreads

Spreads

Spreads

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.

On Monday, the stock market experienced a modest downturn, with the S&P 500 and the Nasdaq Composite retracting from their peak levels despite the surge in technology stocks, fueled by the artificial intelligence boom. The S&P 500 slightly declined by 0.12%, and the Nasdaq fell by 0.41%, even as Nvidia and Super Micro Computer witnessed notable gains. The broader market’s sentiment was tempered by losses in key sectors and major tech companies like Apple and Tesla. Meanwhile, the currency market showed limited volatility as investors awaited significant U.S. economic updates, including Federal Reserve Chair Jerome Powell’s testimony and non-farm payroll data. The anticipation of these events, coupled with mixed outcomes in the stock and currency markets, underscores the cautious approach of investors amidst the ongoing enthusiasm for AI and technology advancements.

On Monday, the stock market experienced a slight retreat, with both the S&P 500 and the Nasdaq Composite stepping down from their all-time highs, despite significant gains in technology stocks spurred by the artificial intelligence boom. The S&P 500 fell by 0.12% to 5,130.95, the Nasdaq Composite dropped by 0.41% to 16,207.51, and the Dow Jones Industrial Average decreased by 97.55 points, or 0.25%, ending at 38,989.83. This pullback brought the S&P 500 and the Nasdaq back from their recent record highs. Noteworthy performances included Nvidia, which surged by more than 3%, and Super Micro Computer, which soared by 18% following the announcement of its upcoming inclusion in the S&P 500. Additionally, bitcoin-related stocks like Microstrategy and Coinbase saw significant gains as the cryptocurrency approached its 2021 peak, indicating a broader appetite for risk among investors.

Despite the excitement around artificial intelligence and select stock advancements, the market was dragged down by underperforming sectors and notable tech companies. The communication services sector led the S&P 500 lower, with Apple dropping 2.5% after a hefty EU antitrust fine and Tesla declining over 7% after announcing new price discounts. Outside of tech, companies like Ford and Macy’s enjoyed gains due to positive sales data and increased acquisition offers, respectively. However, the airline sector showed mixed results, with JetBlue rising over 4% and Spirit Airlines falling more than 10% after canceling their merger plans. As the market digests these movements amid ongoing AI-driven enthusiasm, investors are keenly awaiting insights from Federal Reserve Chair Jerome Powell’s upcoming monetary policy updates, along with key employment and manufacturing data set to be released throughout the week.

Data by Bloomberg

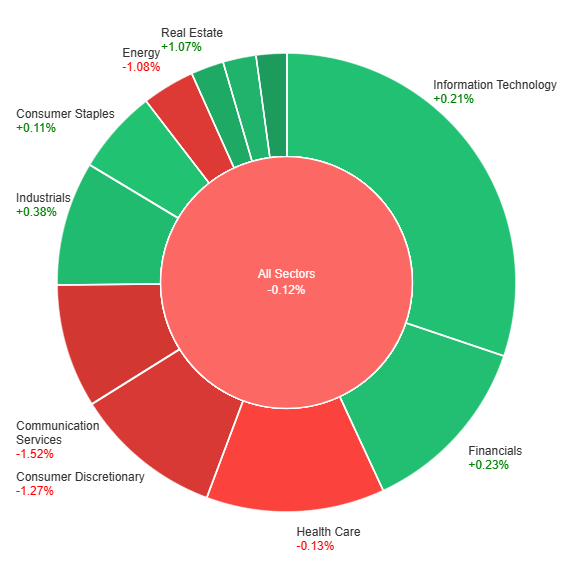

On Monday, the stock market saw a mixed performance across various sectors, with a slight overall decline of 0.12%. Utilities (+1.65%), Real Estate (+1.07%), and Materials (+0.70%) sectors led the gains, showcasing a stronger performance, while Industrials, Financials, Information Technology, and Consumer Staples also posted modest increases. On the downside, Health Care, Energy, Consumer Discretionary, and Communication Services experienced declines, with Communication Services facing the steepest drop of -1.52%. The energy sector also saw a notable decrease of -1.08% and Consumer Discretionary wasn’t far behind with a decline of -1.27%. This varied performance highlights the differing investor sentiments and economic factors influencing each sector.

In the currency market, the USD index displayed minimal volatility, oscillating between 103.72 and 103.96, as market participants braced for a series of pivotal U.S. economic updates. These include the eagerly anticipated non-farm payroll data and Federal Reserve Chair Jerome Powell’s testimony to Congress. Comments from Atlanta Fed President Raphael Bostic highlighted a cautious stance on inflation, suggesting the Fed has the luxury of time to ensure inflation targets are met, while also pointing out the potential inflationary pressures from “pent-up exuberance” within the economy. Furthermore, expectations for Federal Reserve rate adjustments, as inferred from SOFR futures, signal a consensus towards a subdued outlook on rate cuts, anticipated to commence in June, with a projection of nearly -80 basis points through the end of 2024.

In currency pair movements, the EUR/USD saw a modest uptick, gaining 0.17% to reach 1.0860, with market sentiment slightly skewed towards potential gains in anticipation of forthcoming U.S. economic data and Powell’s remarks. Meanwhile, the USD/JPY pair experienced a 0.24% rise to 150.50, amidst expectations of diverging monetary policies between the Fed and the Bank of Japan. The GBP/USD pair also recorded gains, increasing by 0.36% to 1.2698, as traders speculated on the Bank of England maintaining a marginally higher interest rate regime compared to the Fed, amid persistent above-target inflation in the UK. In contrast, Bitcoin and gold witnessed significant appreciation, with Bitcoin surging to a new yearly high of $67.6k, driven by ETF-related buying, and gold advancing by 1.6% to $2,117, both reflecting broader market dynamics and investor sentiment.

| Currency | Data | Time (GMT + 8) | Forecast |

|---|---|---|---|

| USD | ISM Services PMI | 23:00 | 53.0 |

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.