Spreads

Spreads

Spreads

Spreads

Spreads

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.

On Thursday, the Nasdaq Composite achieved a record close at 16,091.92, its highest since November 2021, driven by a surge in tech stocks, particularly those involved in artificial intelligence. This uplift in the stock market saw the S&P 500 also reaching new heights, alongside modest gains for the Dow Jones, marking a continuation of Wall Street’s positive trend into its fourth consecutive month. The enthusiasm around AI and major tech companies has played a pivotal role in this rally, overshadowing concerns about inflation and economic slowdown. Meanwhile, in the currency market, the US Dollar Index saw an upward movement, influencing major currency pairs and setting the stage for watchful anticipation of upcoming economic data and central bank communications. This complex financial landscape, highlighted by tech stock surges and currency fluctuations, encapsulates the dynamic interplay between equity markets and global economic indicators.

On Thursday, the Nasdaq Composite surged to a record close, marking its first since November 2021, by advancing 0.90% to finish at an all-time high of 16,091.92. This rise was significantly buoyed by a rally in tech stocks and chips. The S&P 500 also reached a new record, increasing by 0.52% to end at 5,096.27, while the Dow Jones Industrial Average saw a modest gain of 0.12%, closing at 38,996.39. This upward movement in the stock market concluded February trading on a high note, extending Wall Street’s positive momentum into a fourth consecutive month, despite concerns over the durability of the AI-fueled rally. The Nasdaq led with a 6.12% gain for the month, followed by the S&P 500 with a 5.17% increase, and the Dow with a 2.22% rise, marking its first four-month winning streak since May 2021.

The resurgence of the Nasdaq has been particularly fueled by a wave of enthusiasm for artificial intelligence, significantly lifting major tech stocks, referred to as the “Magnificent 7” (Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla), and subsequently, the broader markets throughout 2023 and into this year. This rally comes after a challenging 2022 characterized by worries over rising interest rates and recession fears. In the specifics of the day’s trading, notable performers included Advanced Micro Devices, which saw a jump of more than 9%, and the VanEck Semiconductor ETF, which closed 2.2% higher. Despite the Federal Reserve’s preferred inflation measure remaining above target in January, it did not exceed Wall Street forecasts, suggesting that consumer spending remains strong. Additionally, while there were setbacks, such as Snowflake’s share drop following the announcement of its CEO’s retirement and disappointing revenue guidance, Okta experienced a significant rise of nearly 23% after reporting strong results.

Data by Bloomberg

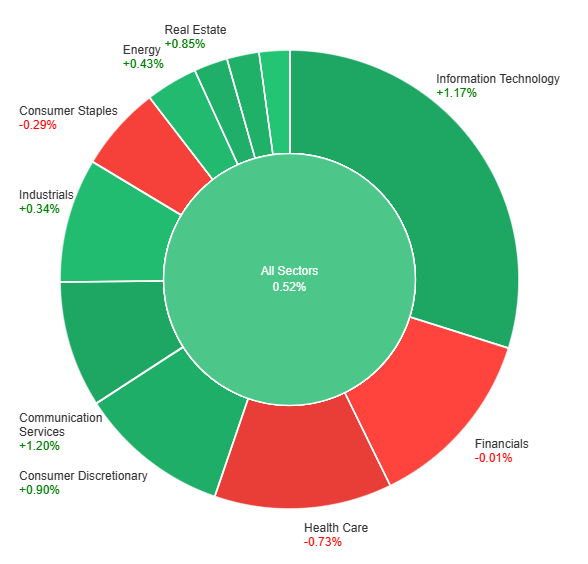

On Thursday, the stock market witnessed a positive overall performance with all sectors combined showing a gain of +0.52%. Leading the gains were Communication Services and Information Technology, up by +1.20% and +1.17% respectively, demonstrating strong investor confidence in these sectors. Other sectors such as Consumer Discretionary, Real Estate, and Materials also posted notable increases, ranging from +0.79% to +0.90%. However, not all sectors fared as well; Utilities showed minimal growth at +0.04%, while Financials slightly declined by -0.01%. The Consumer Staples and healthcare sectors faced downturns, decreasing by -0.29% and -0.73% respectively, indicating areas of investor concern or profit-taking.

The currency market experienced notable movements, with the USD Index (DXY) advancing above the 104.00 barrier, marking its third consecutive session of gains. This strength in the US Dollar influenced various currency pairs, notably pushing the EUR/USD pair to challenge the key support level at 1.0800. The anticipation of economic data releases, including the final S&P Global Manufacturing PMI, Construction Spending, and the ISM Manufacturing PMI, alongside speeches from several Federal Reserve officials, seems to underpin the dollar’s momentum. Furthermore, the currency market is keenly awaiting inflation figures from the euro area, alongside unemployment and manufacturing data, which could influence the EUR/USD trajectory in the coming sessions.

On the other side of the spectrum, the GBP/USD pair faced downward pressure, hinting at a potential move towards the 1.2600 region, influenced by a stronger dollar and upcoming economic releases from the UK. Meanwhile, the USD/JPY pair saw a decline to the 149.20 area, reacting to market speculations about a potential policy shift by the Bank of Japan. The AUD/USD pair also succumbed to the dollar’s strength, breaking below the 0.6500 support level amid concerns over China and forthcoming economic data from Australia. Additionally, the market focus is shifting toward China with the upcoming Manufacturing PMIs, which could have significant implications for the global currency markets, highlighted by a slight drop in the USD/CNH pair to the 7.2100 zone. Amidst these currency shifts, commodities such as WTI oil and precious metals like gold and silver displayed varied performances, adding another layer of complexity to the global financial landscape.

| Currency | Data | Time (GMT + 8) | Forecast |

|---|---|---|---|

| USD | ISM Manufacturing PMI | 23:30 | 49.5 |

| USD | Revised UoM Consumer Sentiment | 23:30 | 79.6 |

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.