Spreads

Spreads

Spreads

Spreads

Spreads

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.

In observance of the Juneteenth holiday, the regular trading session was suspended on Monday, providing investors with a break after a positive week. Despite minor slips on Friday, the S&P 500 and the Nasdaq Composite recorded their best weekly performances since March, with the S&P 500 rising by 2.6% and the Nasdaq adding 3.25%.

The Federal Reserve’s decision to hold off on a June rate hike was well-received by investors, contributing to the market’s upward momentum. While upcoming economic data is limited, investors remain optimistic about the market’s direction as they await the release of housing starts data and prepare for key appearances by Federal Reserve officials.

Fed Chair Jerome Powell’s remarks at a press conference last week indicated that the central bank has yet to finalize its policy decisions ahead of the July meeting. However, the decision to skip a June rate hike broke the Fed’s streak of ten consecutive interest rate increases. Despite the uncertainty surrounding future Fed policy, stocks have continued to rise, reflecting investors’ confidence.

Looking ahead, investors will closely monitor the housing starts data scheduled for release on Tuesday, while also anticipating appearances by New York Fed President John Williams, Fed Vice Chair for Supervision Michael Barr, and Fed Chair Jerome Powell, who is set to testify before Congress later in the week. Additionally, the market will pay attention to the quarterly report from shipping giant FedEx, which will be released after the closing bell on Tuesday.

Data by Bloomberg

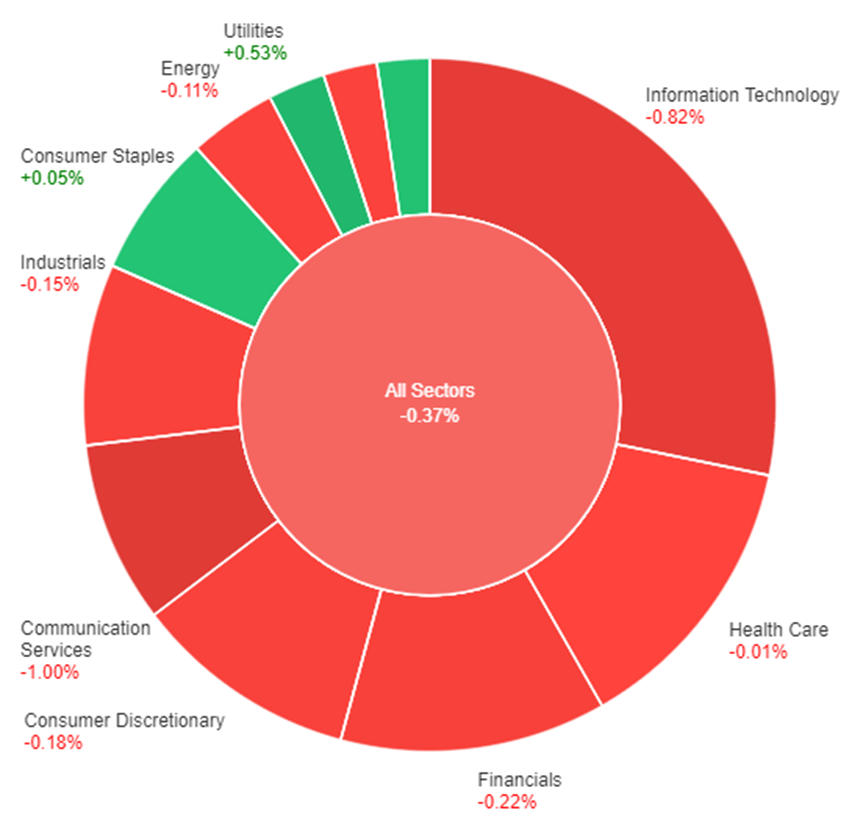

On Friday, the overall performance of the market showed a decline, with all sectors experiencing negative movements except for utilities, materials, and consumer staples. The sectors that saw positive gains were utilities with +0.53%, materials with +0.11%, and consumer staples with +0.05%.

On the other hand, the sectors that recorded losses were health care with -0.01%, energy with -0.11%, real estate with -0.11%, industrials with -0.15%, consumer discretionary with -0.18%, financials with -0.22%, information technology with -0.82%, and communication services with -1.00%. These sectors experienced varying degrees of decline, with information technology and communication services being the hardest hit.

Major Pair Movement

In the currency markets, the British pound (GBP) remains strong despite a slight dip of 0.25%. This comes as good news for the Bank of England (BoE) and inflation, as UK supermarkets report a decrease in food production costs for the first time since 2016. The easing of food price inflation contributes to the positive outlook for the British economy.

Meanwhile, the Australian dollar (AUD) has recovered against the US dollar (USD), rising above the 0.6859 level after reaching a low of 0.6835 on Monday. The AUD/JPY cross also saw a boost, increasing by 0.50% from its lowest point.

The upcoming release of the Reserve Bank of Australia (RBA) minutes is expected to impact market pricing and potentially influence the RBA’s decision regarding interest rates in July. Currently, the market is anticipating a 58% chance of a 25-basis point hike to 4.35%.

Regarding the USD/JPY pair, the uptrend remains intact, but there are concerns about a divergence in the Relative Strength Index (RSI). In thin trading due to a holiday, USD/JPY has held within a narrow range of 141.50-142.00. The Bank of Japan (BoJ) continues to adopt a dovish stance, preventing excessive appreciation of the yen.

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.