Spreads

Spreads

Spreads

Spreads

Spreads

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.

On Wednesday, the stock market showed mixed outcomes, with the Dow Jones and S&P 500 making slight gains, while the Nasdaq Composite faced a decline, influenced by anxiously awaited Nvidia earnings and Federal Reserve insights. Nvidia’s stock dipped ahead of its fiscal report, reflecting investor concerns over its valuation after a significant year-long surge. The market also reacted to Palo Alto Networks’ and SolarEdge Technologies’ disappointing forecasts, alongside the Fed’s minutes indicating a cautious stance on interest rate cuts, emphasizing inflation control. Currency markets saw fluctuations, with the dollar index falling amidst complex global yield dynamics and central bank policies, highlighting the intricate interplay between economic signals, corporate earnings, and monetary policy expectations.

The stock market experienced mixed results on Wednesday, with the Dow Jones Industrial Average slightly gaining by 48.44 points to close at 38,612.24 and the S&P 500 also up by 0.13% at 4,981.80. In contrast, the tech-heavy Nasdaq Composite fell by 0.32%, continuing its downward trend for the third consecutive session, to end at 15,580.87. The market’s attention was particularly focused on Nvidia, ahead of its fiscal fourth-quarter earnings report, amidst growing concerns over the chipmaker’s valuation after its shares surged nearly 230% over the past year. On the day, Nvidia’s stock declined by 2.85%, reflecting investor apprehension about whether it could continue to buoy the market amidst a backdrop of uncertain catalysts for growth.

Market sentiment was further influenced by a combination of corporate news and insights from the Federal Reserve. Palo Alto Networks saw a significant drop of 28.4% after revising its full-year revenue forecast downwards, while SolarEdge Technologies also faced a setback, with its shares falling approximately 12.2% due to weak first-quarter guidance. Adding to the cautious market outlook, minutes from the Federal Reserve’s January meeting revealed a reluctance to cut interest rates anytime soon, emphasizing that any decisions on rate cuts would require greater confidence in the slowing down of inflation. This stance underscores the central bank’s cautious approach to navigating economic signals, leaving the market to look towards corporate earnings and guidance as potential catalysts for future growth.

Data by Bloomberg

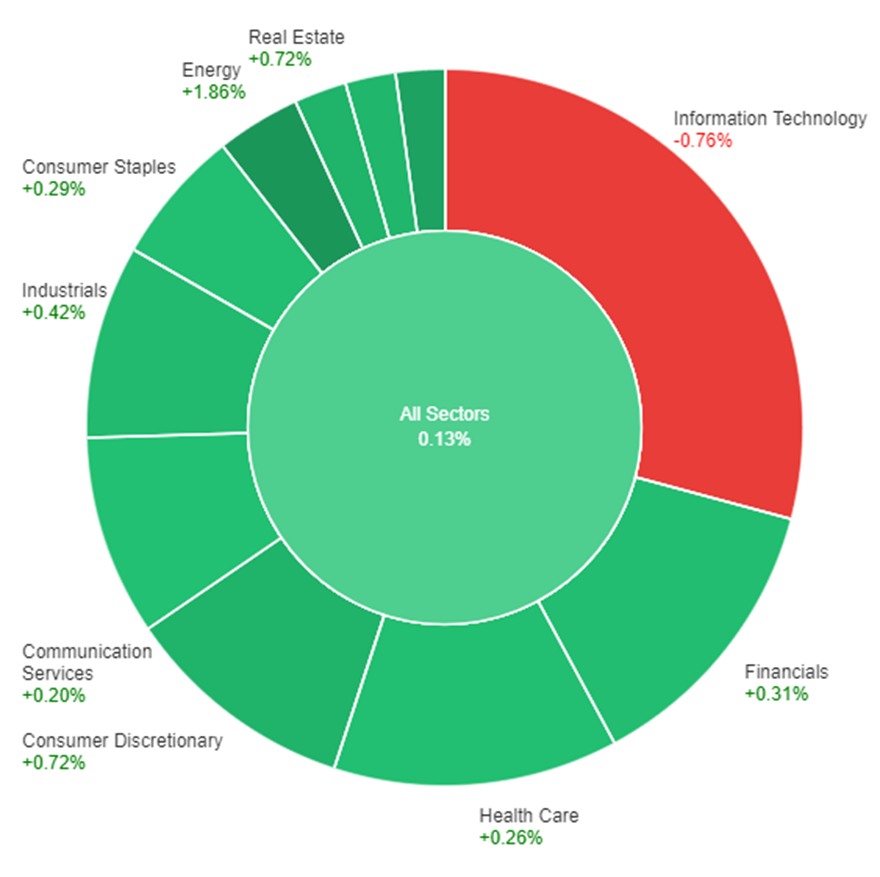

On Wednesday, the market witnessed modest gains across most sectors, with the overall sectors index up by 0.13%. The energy sector led the charge, recording a significant increase of 1.86%, followed closely by utilities, which saw a 1.36% rise. Consumer discretionary and real estate sectors both enjoyed gains of 0.72%, demonstrating a healthy appetite for risk among investors. Other sectors such as materials, industrials, financials, consumer staples, health care, and communication services also experienced growth, albeit at a more moderate pace. However, the information technology sector bucked the positive trend, facing a downturn of 0.76%, indicating sector-specific challenges or profit-taking by investors.

The currency market experienced notable fluctuations, with the dollar index declining by 0.9% amid a complex interplay of treasury yields and central bank policies. The increase in Treasury yields, although outpaced by European yields, failed to keep up with the steadiness of Japanese Government Bond (JGB) yields. This dynamic, alongside the diminishing likelihood of interest rate cuts by major central banks such as the Federal Reserve (Fed), the European Central Bank (ECB), and the Bank of England (BoE), exerted pressure on risk appetite. The anticipation surrounding the Federal Reserve’s minutes and Nvidia’s report further influenced market sentiments. Despite the anticipation, the Fed minutes merely echoed previous statements and comments, offering no new impetus for dollar strength. Meanwhile, the USD/JPY pair saw a slight increase, attributed to the static nature of JGB yields which made the yen less attractive compared to its higher-yielding counterparts.

In Europe, the ECB’s stance, as articulated by Pierre Wunsch, suggested a prolonged period of tight monetary policy, given the persistent wage pressures and tight labor markets. This position was mirrored by the market’s adjustment in expectations for rate cuts, with the first ECB rate reduction now fully priced in for June. The euro found some support against the dollar, benefiting from a tightening in the 2-year bund-Treasury yield spreads. However, the recovery of the EUR/USD pair was tempered by technical resistance and a cautious outlook for the BoE’s policy direction, which also impacted the GBP/USD pair. The British pound struggled against the backdrop of rising Gilts-Treasury yield spreads and comments from BoE officials emphasizing the cost of delayed rate adjustments. These developments underscore the intricate balance of yield dynamics, central bank policies, and economic indicators shaping the currency markets, with implications for the path of the dollar and its major counterparts.

| Currency | Data | Time (GMT + 8) | Forecast |

|---|---|---|---|

| EUR | French Flash Manufacturing PMI | 16:15 | 43.5 |

| EUR | French Flash Services PMI | 16:15 | 45.7 |

| EUR | German Flash Manufacturing PMI | 16:30 | 46.1 |

| EUR | German Flash Services PMI | 16:30 | 48.0 |

| GBP | Flash Manufacturing PMI | 17:30 | 47.5 |

| GBP | Flash Services PMI | 17:30 | 54.2 |

| USD | Unemployment Claims | 21:30 | 217K |

| USD | Flash Manufacturing PMI | 22:45 | 50.5 |

| USD | Flash Services PMI | 22:45 | 52.4 |

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.