Spreads

Spreads

Spreads

Spreads

Spreads

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.

Despite the S&P 500, Dow Jones, and Nasdaq reaching new peaks amidst the consumer price index (CPI) rising as anticipated, the market remains divided in response. Analysts note both bullish and bearish sentiments, with investors bracing for potential strategic investment opportunities. Oracle’s 12% decline and Macy’s 8% drop affect sector dynamics, while currency markets respond subtly to the CPI data, keeping the dollar index down. The Fed’s impending policy announcement and cues from Jerome Powell’s commentary are anticipated, influencing future rate adjustment speculations. Meanwhile, diverse currency pairs show varied movements, indicating nuanced market shifts, while attention turns to forthcoming events like US retail sales and central bank meetings impacting currency markets’ cautious stance.

The stock market saw a continued climb as the S&P 500, Dow Jones Industrial Average, and Nasdaq Composite all rose, hitting new 52-week highs. This growth occurred despite the consumer price index (CPI) rising 3.1% year over year in November, matching economist predictions. However, the month-over-month CPI increase aligned with expectations, maintaining a steady inflation trajectory. Analysts noted that while both bullish and bearish sentiments exist about the CPI figures, the market largely responded in a manner consistent with expectations, with many investors anticipating a potential dip for strategic investments.

Investors are eagerly awaiting the Federal Reserve’s upcoming policy announcement, anticipated to maintain steady interest rates. However, the market is keenly attentive to cues from Chair Jerome Powell’s commentary, seeking indications about potential future rate adjustments. Amidst this market climate, Oracle shares dropped by over 12% due to lower-than-expected fiscal second-quarter revenue, while Macy’s declined by 8% following a downgrade to sell from Citi, impacting the market’s sectoral dynamics.

Data by Bloomberg

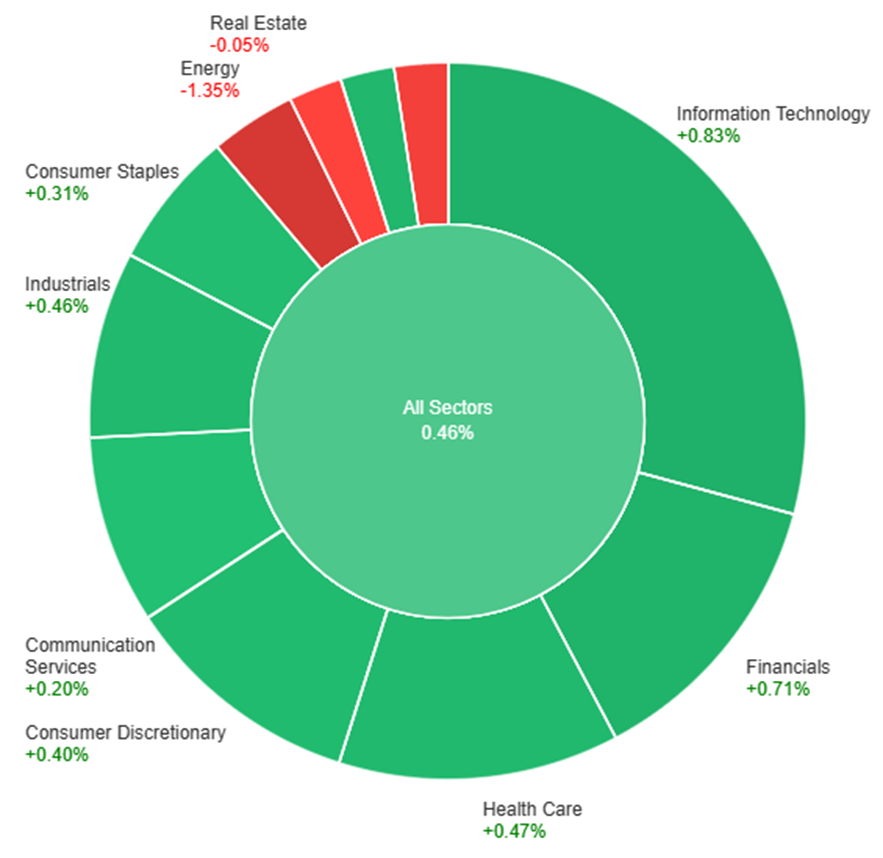

On Tuesday, most sectors experienced gains, with the overall market rising by 0.46%. The Information Technology sector led the gains with an increase of 0.83%, followed by Financials at 0.71% and Materials at 0.57%. Health Care and Industrials also saw positive movement, each rising by 0.47% and 0.46%, respectively. However, sectors like Energy, Utilities, and Real Estate faced declines, with Energy notably dropping by 1.35%. Utilities and Real Estate experienced smaller decreases of 0.41% and 0.05%, respectively, marking a mixed day across various sectors.

The recent currency market updates reveal a nuanced response to the US CPI data, maintaining the dollar index down by 0.22%. Core inflation figures persisting at 4% year-on-year hindered a dovish Fed pivot signal, despite real weekly earnings experiencing a significant 0.5% surge in the month. This upturn in earnings, especially in super core services minus shelter costs, influenced Powell’s outlook, contributing to a marginal rise in Treasury yields and the dollar post-CPI.

EUR/USD witnessed a 0.24% uptick, benefiting from a weaker dollar, declining energy prices, optimistic indicators in Germany’s ZEW expectations index, and tightened bund treasury yield spreads. However, the currency pair is seeking support above specific moving averages to solidify its sizable speculative long position. Meanwhile, USD/JPY experienced a 0.4% drop from recent lows, navigating towards equilibrium after a notable November-December plunge, a portion of it attributed to an exaggerated Fed rate cut and unrealistic BoJ rate hike expectations. The overall trend remains in favor of shorts unless key resistance at 147.76 is breached, considering the historical context of a double-top formation from 2022/23 and the anticipated reversal of the Fed rate hike cycle.

The sterling remained relatively stagnant amid concerns over decelerating UK wage growth and domestic political uncertainty. Looking ahead, market attention shifts to upcoming events such as US retail sales and the ECB and BoE meetings, viewed as preludes to anticipated rate adjustments by March and June, respectively, maintaining a cautious stance in the currency markets.

| Currency | Data | Time (GMT + 8) | Forecast |

|---|---|---|---|

| GBP | GDP m/m | 15:00 | -0.1% |

| USD | Core PPI m/m | 21:30 | 0.2% |

| USD | PPI m/m | 21:30 | 0.0% |

| USD | Federal Funds Rate | 03:00 (14th) | 5.50% |

| USD | FOMC Statement | 03:00 (14th) | |

| USD | FOMC Press Conference | 03:30 (14th) | |

| NZD | GDP q/q | 05:45 (14th) | 0.2% |

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.