Spreads

Spreads

Spreads

Spreads

Spreads

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.

In the stock market, October witnessed surging interest rates, leading to a challenging month for investors, but there was a modest recovery on Tuesday as major indices rebounded. Real estate and financial sectors outperformed, while some tech giants faced declines. Despite recent gains, it marked the third consecutive losing month for major stock indices, driven by rising Treasury yields. The currency market saw the US dollar strengthen, particularly against the yen, influenced by central bank policies and economic data. As the markets watch for signals from the Federal Reserve and other central banks, investors remain cautious yet hopeful for a year-end rally, with an eye on currency pairs, such as USD/JPY and EUR/USD.

In the stock market, October was marked by surging interest rates, leading to a challenging month for investors. However, on Tuesday, there was a modest recovery as the major indices rebounded. The S&P 500 climbed 0.65% to 4,193.80, and the Nasdaq Composite added 0.48% to 12,851.24, while the Dow Jones Industrial Average advanced 0.38% to 33,052.87. Notably, real estate and financial sectors outperformed, with gains of 2% and 1.1%, respectively, while some mega-cap tech stocks, such as Alphabet and Meta Platforms, faced declines. The Cboe Volatility Index (VIX) dropped below its long-term average, indicating reduced market uncertainty. Earnings reports also played a role in market movements, with Caterpillar’s stock sliding more than 6% due to a modest fourth-quarter revenue outlook, and JetBlue shares dropping over 10% as the airline’s third-quarter results fell short of expectations.

Despite the recent gains, October marked the third consecutive losing month for major stock indices. The Dow and S&P 500 fell 1.4% and 2.2%, respectively, while the tech-heavy Nasdaq declined by 2.8%. These losses were driven by a rapid increase in Treasury yields, with the 10-year U.S. Treasury yield reaching a significant 5% level, last seen in 2007. Market participants attribute this rise to concerns that the Federal Reserve may maintain higher interest rates for an extended period. The Fed’s upcoming decision on interest rates is eagerly anticipated, with expectations that the central bank will likely keep rates unchanged. Investors are looking for signals of a more dovish stance from the Fed to relieve downward pressure on rates and support a sustainable stock market rebound. Additionally, traders are hopeful for seasonal tailwinds in November, historically a strong month for markets, but they believe that a peak in bond yields will be necessary for a year-end rally.

Data by Bloomberg

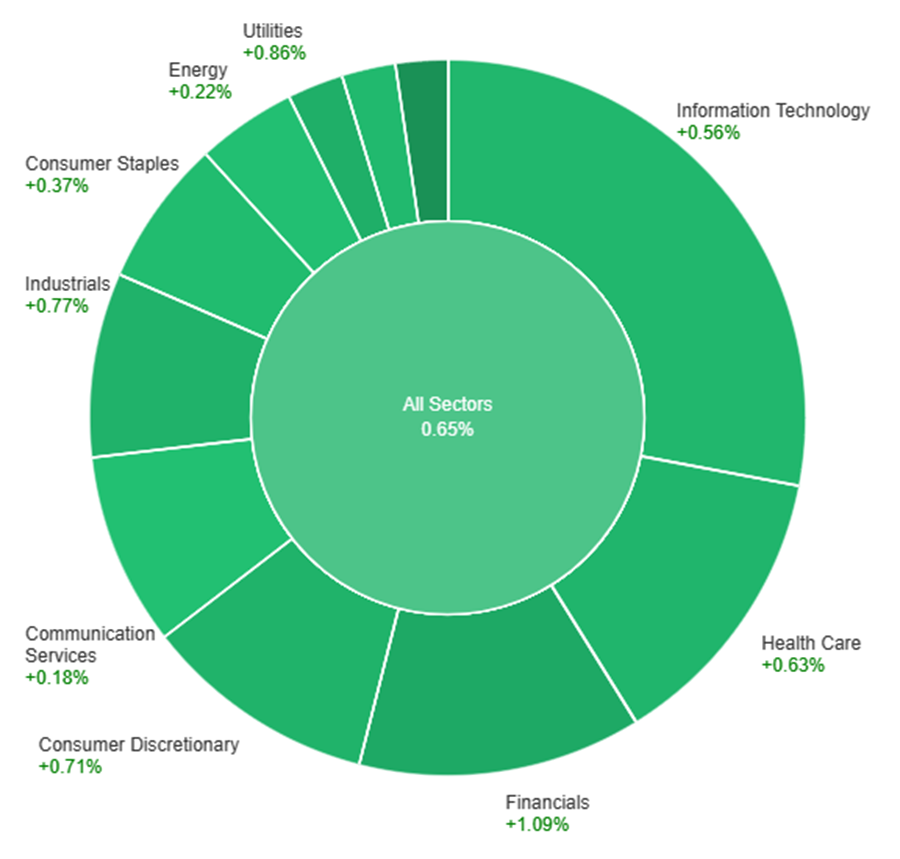

On Tuesday, the overall market showed a positive trend, with all sectors collectively gaining 0.65%. Among the sectors, Real Estate led the way with an impressive increase of 2.04%, followed by Financials at 1.09% and Utilities at 0.86%. Other sectors, such as Industrials, Consumer Discretionary, and Health Care, also experienced gains ranging from 0.63% to 0.77%. However, Information Technology, Materials, Consumer Staples, Energy, and Communication Services had more modest increases, ranging from 0.18% to 0.56%.

In recent currency market developments, the US dollar demonstrated strength as the dollar index saw a 0.6% increase, primarily driven by a remarkable 1.6% surge in USD/JPY, nearing its 2022 peak. This surge was attributed to the Bank of Japan’s (BoJ) shift away from ultra-easy monetary policies, perceived by many as too little and too late in comparison to substantial rate hikes by other major central banks worldwide. Additionally, the US dollar gained broader traction following positive economic data from the United States. The U.S. employment cost index, home prices, and consumer confidence all exceeded expectations, leading to a 7-basis-point rise in 2-year Treasury yields, a 4-basis-point increase on the day. Conversely, the euro lost ground against the US dollar, falling 0.4%, as euro zone inflation and GDP figures came in slightly weaker than forecasts. This decline was further exacerbated by a narrowing of 2-year bund-Treasury yield spreads. Looking ahead, the currency market is keeping a watchful eye on developments like the ECB’s potential rate cuts, as well as any hints of changes in the Federal Reserve’s stance, which could impact the future direction of the EUR/USD pair.

In particular, USD/JPY made a remarkable 1.66% jump, reaching new highs for 2023 at 151.715, approaching the 32-year peak from October 21, 2022, at 151.94. This upward momentum raised concerns of potential pullback risks, particularly due to the narrowing of Treasury-JGB yield spreads as USD/JPY hit new highs. Traders may consider taking profits if the currency pair fails to close above the 2022 high. However, an unobstructed breakout could lead to a potential target at 155.19, representing the 161.8% Fibonacci retracement off the base from 2023 and exacerbating Japan’s imported inflation concerns. Meanwhile, USD/CAD rose by 0.4% to reach new highs for 2023, primarily influenced by recessionary GDP data. The Australian dollar fell by 0.6%, partially due to disappointing factory data from China, which also pushed USD/CNH close to October’s highs. Finally, the global market experienced lower prices for oil and copper, reflecting concerns about global economic growth risks. These factors collectively indicate an evolving landscape in the currency market, with central bank policies, economic data, and geopolitical factors playing significant roles in shaping the future direction of major currency pairs.

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.