Spreads

Spreads

Spreads

Spreads

Spreads

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.

Major stock indices, including the Dow Jones Industrial Average, S&P 500, and Nasdaq Composite, saw modest gains as investors awaited U.S. consumer inflation figures and monitored Treasury yields’ retreat. The market was also influenced by expectations of the consumer price index report and Federal Reserve policy, while Exxon Mobil announced a significant acquisition and Birkenstock faced a challenging market debut. Geopolitical tensions in Israel and Hamas contributed to market uncertainty. In the currency market, the US Dollar remained flat despite positive wholesale inflation data and FOMC minutes, with the focus shifting to the impending Consumer Price Index release and divergent views among committee members. The US Dollar Index and Treasury yields experienced minor fluctuations, while currency pairs like EUR/USD and GBP/USD demonstrated varied behavior. Gold and Silver rallied due to lower yields and a weakened US Dollar.

In Wednesday’s stock market, major indices saw modest gains as investors eagerly awaited the release of the new U.S. consumer inflation figures, while Treasury yields continued their retreat. The Dow Jones Industrial Average rose by 0.19%, or 65.57 points, closing at 33,804.87. The S&P 500 experienced a 0.43% increase, ending the day at 4,376.95, while the Nasdaq Composite, dominated by tech stocks, surged 0.71% and closed above its 50-day moving average for the first time since September 14. This marked the fourth consecutive day of gains for these key indices. Investors were also anticipating the consumer price index report for September, with economists predicting a 0.3% increase from the previous month and a year-over-year rise of 3.6%. This data was seen as critical for insights into future Federal Reserve policy moves, especially after the recent revelation of hotter-than-expected wholesale inflation figures. Additionally, the release of minutes from the Fed’s September meeting indicated that a majority of officials believed one more interest rate hike was likely, with rising Treasury yields playing a significant role in their considerations.

On the corporate front, Exxon Mobil announced the acquisition of shale driller Pioneer Natural Resources in an all-stock deal worth $59.5 billion, marking the largest merger announced on Wall Street in the year. Meanwhile, sandal manufacturer Birkenstock faced a challenging market debut, with shares priced at $46 each but falling to $40.20 by the close of the session. Investors were also monitoring the ongoing conflict between Israel and Hamas, as the latter launched an attack on Israeli civilians, leading to the deadliest offensive in the region in five decades. President Joe Biden condemned the attacks as terrorism and expressed unwavering support for Israel. Overall, the market sentiment appeared uncertain, with conflicting factors such as inflation, interest rates, and geopolitical tensions contributing to the mixed outlook for stocks.

Data by Bloomberg

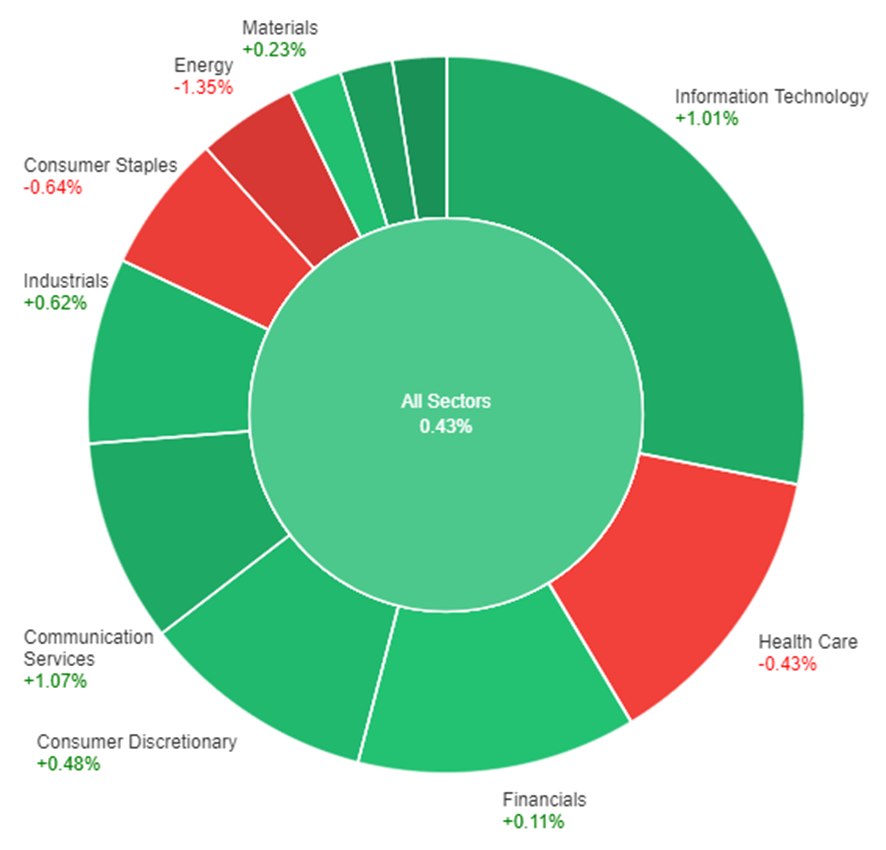

On Wednesday, the performance of various sectors in the market showed mixed results. Overall, all sectors combined saw a modest increase of 0.43%. Among the sectors, Real Estate performed exceptionally well with a gain of 2.01%, followed by Utilities at 1.63%, and Communication Services at 1.07%. Information Technology and Industrials also had positive gains at 1.01% and 0.62%, respectively. Meanwhile, Consumer Discretionary and Materials had smaller gains at 0.48% and 0.23%. On the other hand, Financials and Health Care experienced minimal gains of 0.11% and a decline of -0.43%, respectively. Consumer Staples and Energy were the worst-performing sectors, with losses of -0.64% and -1.35%, respectively.

In the recent currency market updates, the US Dollar remained largely flat despite unexpected positive data on US wholesale inflation and the release of the Federal Open Market Committee (FOMC) minutes. The Greenback’s weakness persisted as US Treasury yields continued to retreat, and a risk-on sentiment in the Wall Street stock market failed to provide support. Notably, the US Producer Price Index (PPI) accelerated in September, surprising analysts by rising from 2.0% to 2.2%, as compared to the expected 1.6%. However, this development did not raise significant concerns, with all eyes turning to the impending release of the Consumer Price Index (CPI), expected to decrease from 3.7% to 3.6% in September, promising heightened volatility in the currency market. Furthermore, the FOMC minutes revealed divergent perspectives among committee members, emphasizing a data-dependent approach and the necessity of a substantial rebound in inflation to reach a consensus on further interest rate hikes.

Following the FOMC minutes, the US Dollar Index (DXY) experienced a slight pullback but managed to finish flat at 105.75, rebounding from strong support at 105.50. The US Treasury yield for 10-year bonds dropped to 4.55%. Notably, EUR/USD maintained its recent gains and stayed close to a strong resistance level at 1.0630, demonstrating a bullish tone. However, with a week of continuous ascent, the pair appeared poised for a consolidation phase, pending the release of the US CPI figures. Meanwhile, GBP/USD achieved a second consecutive daily close above the 20-day Simple Moving Average, hovering around 1.2300 and indicating signs of potential fatigue in its recovery. Key economic data releases are expected in the UK on Thursday. In addition, Gold and Silver rallied, benefiting from lower yields and a weakened US Dollar, breaking above $1,860 and $22.00, respectively.

| Currency | Data | Time (GMT + 8) | Forecast |

|---|---|---|---|

| GBP | Gross Domestic Product | 14:00 | 0.2% |

| USD | Consumer Price Index | 20:30 | 0.3% |

| USD | Core Consumer Price Index | 20:30 | 0.3% |

| USD | Unemployment Claims | 20:30 | 211K |

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.