Spreads

Spreads

Spreads

Spreads

Spreads

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.

The S&P 500 experienced a 0.3% decline driven by concerns over rising Treasury yields and upcoming remarks from Federal Reserve Chairman Jerome Powell. The decline was also impacted by a drop in banking and retail shares. The Dow Jones Industrial Average followed suit, slipping by 0.5% to 34,288.83, while the Nasdaq Composite managed a small gain at 13,505.87. Notably, Nvidia’s stock dipped 2.9%, offsetting an earlier increase.

Bank ratings adjustments and challenging operating conditions caused several banks, both regional and larger, to witness declines. Consequently, the financial sector saw a 0.9% drop, making it the day’s poorest-performing sector within the S&P 500. Major banks like KeyCorp, Comerica, and JPMorgan Chase faced declines of 4.1% and 2.1% respectively. Meanwhile, Dick’s Sporting Goods and Macy’s tumbled by 24% and 14%, leading to a downward trajectory for the SPDR S&P Retail ETF. Nike also recorded over a 1% slide, marking its ninth successive daily loss. Wall Street’s attention has been on the bond market, particularly the 10-year Treasury yield, which reached its highest point since 2007 during the week. The yield dipped slightly to 4.33% on Tuesday.

Market analysts anticipate a continued market pullback. They point to the influence of climbing yields and a cautious consumer sentiment as drivers of this trend. Investors are eagerly awaiting Federal Reserve Chairman Jerome Powell’s speech at the Jackson Hole economic symposium on Friday, which is expected to provide insights into the central bank’s future monetary policy decisions.

Data by Bloomberg

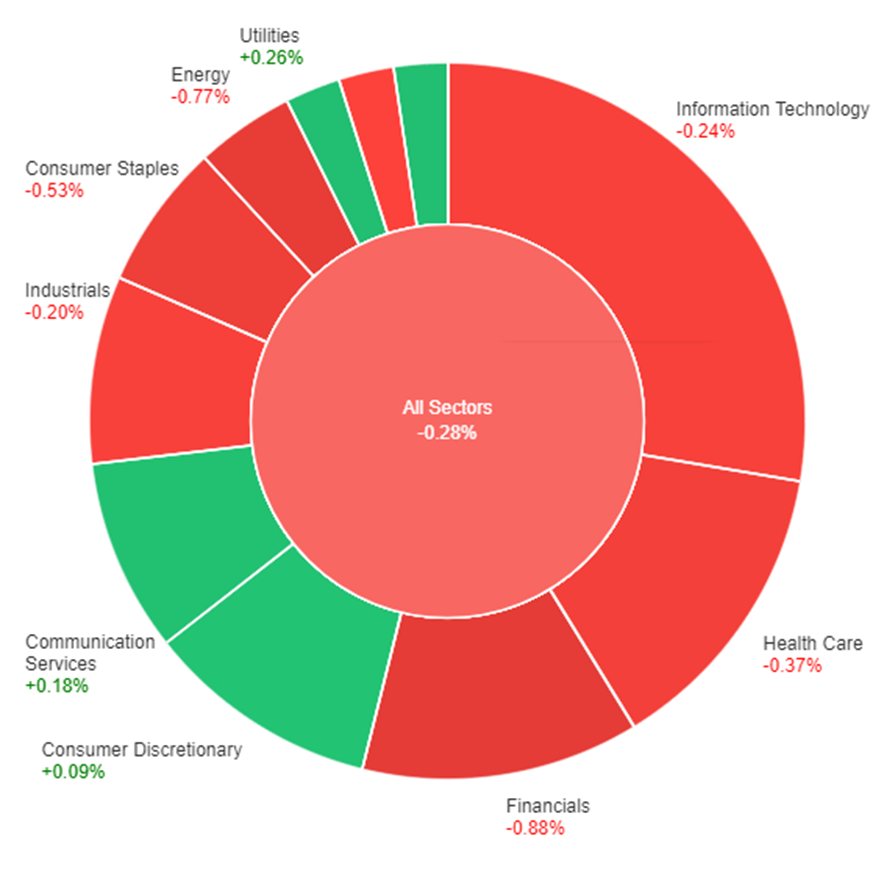

On Tuesday, most sectors experienced a slight decline, with the overall market slipping by 0.28%. The Real Estate sector managed a 0.28% gain, while Utilities and Communication Services saw increases of 0.26% and 0.18% respectively. On the positive side, Consumer Discretionary showed a marginal uptick of 0.09%. However, several sectors faced losses, including Energy and Financials, which saw declines of 0.77% and 0.88% respectively. The Consumer Staples sector had the largest drop at 0.53%, followed by Health Care at 0.37%, Information Technology at 0.24%, and Industrials at 0.20%.

The dollar index exhibited a 0.24% increase, led by a 0.36% decline in EUR/USD, pushing the euro close to breaking its pivotal lows from July. The possibility of this break is tied to Federal Reserve Chair Jerome Powell’s upcoming speech at Jackson Hole and the potential for its content to align with statements from Richmond Fed President Barkin. Despite a temporary alleviation from recent events that might have contributed to the Treasury yield’s retreat from post-GFC highs, the 2-year bund-Treasury yield spreads hit new lows for 2023. This shift coincided with the Treasury curve inverting further due to the attraction of high 10-year yields and short-covering. Barkin’s comments, which deviated from his generally dovish stance, introduced the risk that Powell could emphasize relative U.S. economic strength and the importance of achieving the Fed’s 2% inflation mandate.

The uncertainty centers on the potential length of elevated interest rates by the Fed and the implications for inflation. The conversation also includes evaluating the impact of China’s economic challenges. Jens Eskelund, President of [unspecified institution], weighed in on these matters. Despite the Fed’s stance based on strong economic growth and a tight labor market, both S&P and Moody’s have expressed concerns, leading to a market prediction of almost 100 basis points of Fed rate cuts next year, coinciding with one of the most rapid rate increases in decades. The USD/JPY pair dropped by 0.25%, reflecting a retreat in Treasury yields, while sterling faced a 0.13% decline due to factors including the dollar’s broader rebound from Barkin’s comments and an equities pullback. USD/CNH saw a 0.22% rise, in contrast to USD/CNY’s 0.09% gain. The focus now shifts to the global PMIs scheduled for Wednesday and Powell’s upcoming presentation on Friday.

| Currency | Data | Time (GMT + 8) | Forecast |

|---|---|---|---|

| EUR | French Flash Manufacturing PMI | 15:15 | 45.1 |

| EUR | German Flash Services PMI | 15:15 | 47.5 |

| EUR | Flash Manufacturing PMI | 15:30 | 38.9 |

| EUR | Flash Services PMI | 15:30 | 51.5 |

| GBP | Flash Manufacturing PMI | 16:30 | 45.1 |

| GBP | Flash Services PMI | 16:30 | 50.9 |

| USD | Flash Manufacturing PMI | 21:45 | 48.9 |

| USD | Flash Services PMI | 21:45 | 52.1 |

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.