Spreads

Spreads

Spreads

Spreads

Spreads

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.

Stock markets experienced a significant decline on Tuesday, driven by mounting apprehensions about the global economy, particularly China, and a downturn in the U.S. banking sector. The Dow Jones Industrial Average dropped by 361.24 points, or 1.02%, closing at 34,946.39, ending its three-day positive streak. The S&P 500 retreated by 1.16%, closing at 4,437.86, slipping below its 50-day moving average, which could signal the initiation of a potential downtrend. The Nasdaq Composite also recorded a 1.14% fall, concluding the day at 13,631.05.

In the U.S., financial stocks saw a notable weakening. JPMorgan Chase and Wells Fargo shares both declined by 2%, while Bank of America shares dropped by 3%. This decline followed a warning from Fitch that it might downgrade the credit rating of numerous banks, including JPMorgan Chase. Just the previous week, Moody’s had already downgraded the ratings of ten U.S. banks and placed several major institutions on a watchlist for potential downgrades. Regional banks faced a similar fate, with the SPDR S&P Regional Banking ETF (KBE) experiencing a 3% decline. This decrease came after Minneapolis Federal Reserve President Neel Kashkari advocated for more stringent capital regulation.

Global investor sentiment was further impacted by discouraging economic data from China, combined with an unexpected interest rate cut by its central bank. China reported a mere 3.7% increase in industrial production in July compared to the previous year, falling short of expectations. Retail sales growth was also underwhelming, prompting the People’s Bank of China to reduce interest rates by 15 basis points to 2.5%. However, this move failed to allay concerns and instead intensified worries about China’s ailing real estate market. Market experts suggested that skepticism was growing about the effectiveness of Chinese government stimulus measures, contributing to the overall market unease.

The stock market’s turbulence coincided with a week marked by prominent earnings reports from major retailers. Home Depot exceeded analyst expectations, reporting higher earnings per share and revenue, which provided a slight boost to its stock. The week ahead also promised releases from Target and Walmart, further shaping investor sentiment. On the data front, July’s U.S. retail sales figures surprised economists, with a 0.7% month-over-month increase, surpassing the estimated 0.4% rise. These developments highlighted a robust consumer outlook amidst the broader economic uncertainties.

Data by Bloomberg

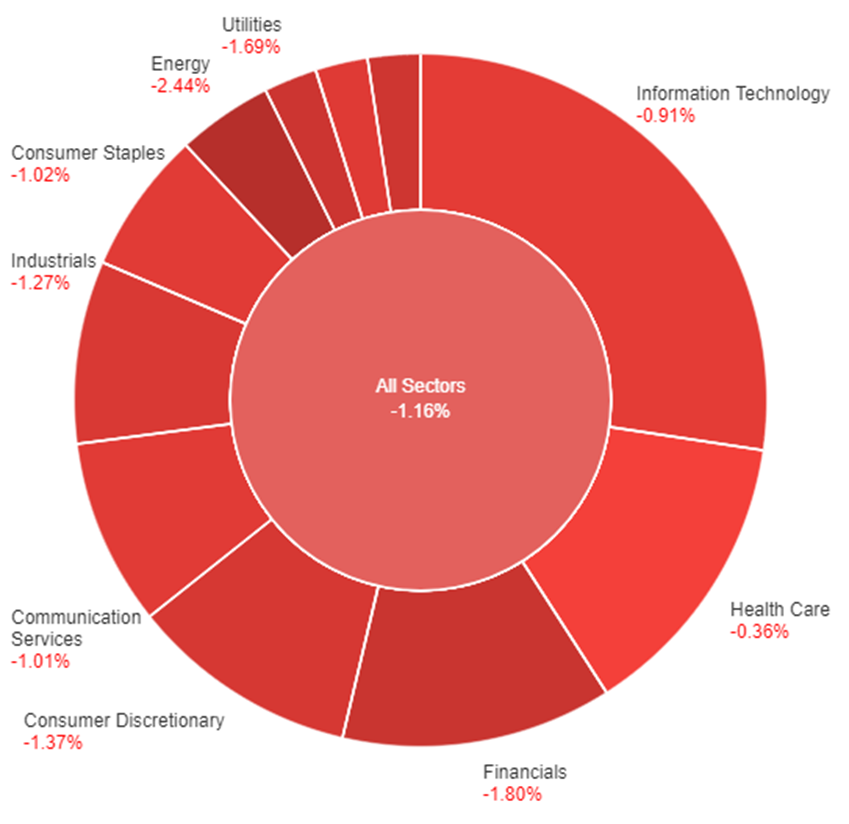

On Tuesday, the stock market witnessed widespread declines across all sectors, with a notable decrease of 1.16%. Among the sectors, Energy suffered the most significant drop, plummeting by 2.44%, while Financials and Utilities also experienced substantial declines of 1.80% and 1.69%, respectively. Consumer Discretionary and Materials sectors faced losses of 1.37% and 1.65%, highlighting a challenging day for these segments. Industrials and Real Estate both slid by 1.27% and 1.07%, respectively. Communication Services and Consumer Staples followed suit with decreases of 1.01% and 1.02%. Information Technology encountered a decline of 0.91%, while Health Care demonstrated relatively milder losses of 0.36%.

Major Pair Movement

The US Dollar Index extended its strength, marking a fourth successive daily gain and reaching a one-month peak on Tuesday. This recovery was driven by increased risk aversion and a rebound in Treasury yields. Wall Street stocks faced over a 1% decline, while US 10-year Treasury yields initially dropped but later rebounded above 4.20%. Meanwhile, the US Retail Sales surpassed expectations by rising 0.7% in July, exceeding the projected 0.2%. However, the NY Empire Manufacturing Index decreased to -19 from -1. Upcoming economic indicators include Building Permits, Housing Starts, and Industrial Production, with particular attention on the forthcoming FOMC meeting minutes.

EUR/USD initially rose to 1.0950 before retreating to 1.0900, influenced by a resurgent US Dollar. Eurozone data on GDP, Employment, and Industrial Production will be unveiled on Wednesday. In the UK, robust wage data fueled expectations of a Bank of England (BoE) rate hike, boosting the Pound. GBP/USD steadily advanced, closing above 1.2700. The UK’s upcoming Consumer Price Index (CPI) inflation report for July will be closely monitored, with an anticipated decline from 7.9% to 6.7%.

USD/JPY remained stable around 145.50, testing support near 146.00 but finding strength above 145.00. Canada witnessed a rebound in its Consumer Price Index to 3.3% in July, surpassing the expected 3%, briefly lifting the Canadian Dollar. USD/CAD sustained its upward trend, closing just below 1.3500.

Economic Data

| Currency | Data | Time (GMT + 8) | Forecast |

|---|---|---|---|

| NZD | Official Cash Rate | 10:00 | 5.50% (Actual) |

| NZD | RBNZ Press Conference | 11:00 | 0.9% |

| GBP | CPI y/y | 14:00 | 6.7% |

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.