Spreads

Spreads

Spreads

Spreads

Spreads

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.

On Monday, US stocks rebounded with the S&P 500 and Nasdaq Composite both gaining ground. The broader market index rose 0.58%, closing at 4,489.72, while the Nasdaq surged by 1.05% to end at 13,788.33. In contrast, the Dow Jones Industrial Average edged up 0.07%, finishing at 35,307.63.

Nvidia, a key chip company, saw a notable resurgence, its shares climbing 7.1% after an 8.5% slump the prior week. The boost came from Morgan Stanley reaffirming Nvidia as a top pick ahead of its earnings report. Other chip stocks followed suit, with the VanEck Semiconductor ETF (SMH) up 3%, despite a more than 6% decline in August.

These gains unfolded amid a recent struggle for stocks to maintain momentum in the latter part of 2023’s summer. While the S&P 500 and Nasdaq faced declines of 0.3% and 1.9% respectively in the previous week, the Dow bucked the trend, posting a 0.6% gain in the same period – its fourth positive week in five.

Looking ahead, the upcoming week was poised to provide insights into the US consumer’s state, with anticipated earnings reports from major companies like Home Depot, Target, and Walmart, along with the release of July’s retail sales data. These reports followed mixed inflation data from the previous week, which showed a moderated yet still elevated price increase above the Federal Reserve’s 2% target.

Data by Bloomberg

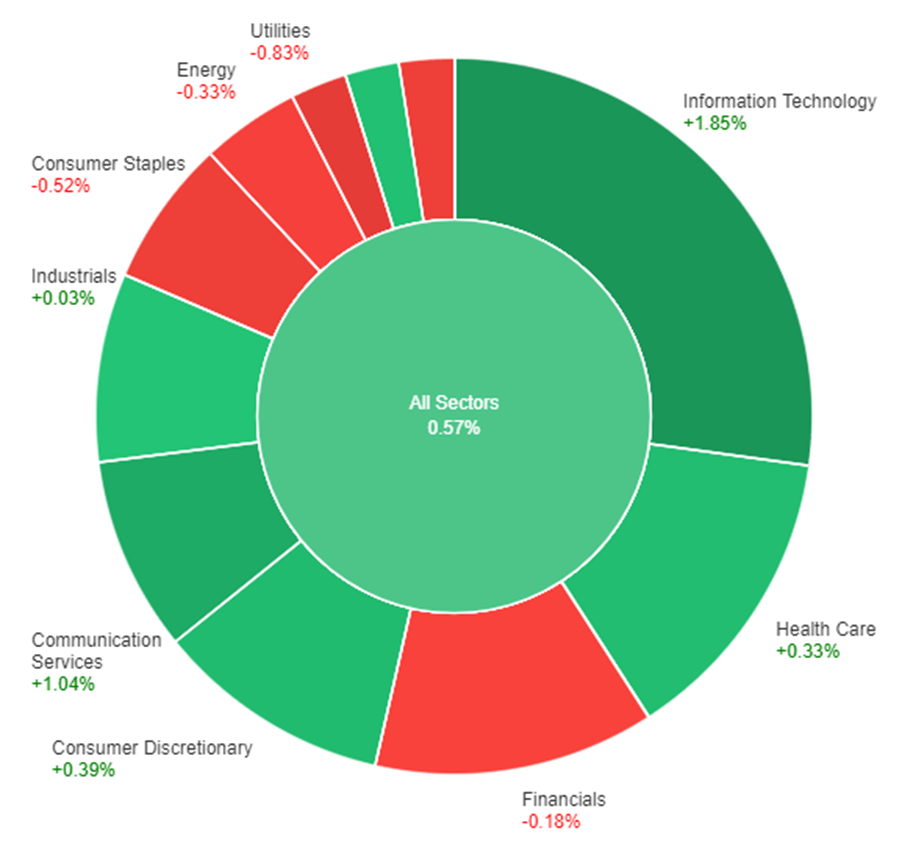

On Monday, the US stock market exhibited varied sectoral performance. The overall market saw a positive movement of 0.57%. The Information Technology sector led the gains with an impressive 1.85% increase, followed by Communication Services at +1.04%, and Consumer Discretionary at +0.39%. Health Care and Materials sectors also contributed positively, rising by 0.33% and 0.19% respectively. However, some sectors experienced slight gains or remained nearly unchanged, including Industrials (+0.03%).

On the other hand, several sectors faced declines. Financials registered a decrease of -0.18%, Energy was down by -0.33%, while Consumer Staples and Real Estate both experienced more pronounced declines at -0.52% and -0.54% respectively. The Utilities sector saw the most significant decrease, ending the day with a decline of -0.83%.

Major Pair Movement

The US Dollar Index achieved its highest daily close in over a month, surpassing 103.15, supported by rising US yields even as the Federal Reserve’s stability is expected. Retail Sales data and NY Empire Manufacturing Index awaited. The Euro faced fluctuations, briefly dipping below 1.0900 but recovering, while GBP/USD stabilized around 1.2700 after hitting 1.2616, accompanied by the upcoming UK employment and inflation reports.

USD/JPY extended gains, reaching its highest daily close near 145.50 since November. Japan’s Q2 GDP and Industrial Production data anticipated. USD/CHF hit a one-month peak before retreating, with Swiss Producer and Import Price Index due. USD/CAD maintained an upward trend above 1.3400 ahead of Canada’s CPI report. AUD/USD declined for a fifth day due to commodity drops, RBA minutes expected. NZD/USD hit a November-low close below 0.6000 ahead of the RBNZ decision. Gold and Silver slid but stabilized, Gold above $1,900 and Silver around $22.55.

Economic Data

| Currency | Data | Time (GMT + 8) | Forecast |

|---|---|---|---|

| AUD | Monetary Policy Meeting Minutes | 09:30 | |

| AUD | Wage Price Index q/q | 09:30 | 0.9% |

| GBP | Claimant Count Change | 14:00 | 19.6K |

| CAD | CPI m/m | 20:30 | 0.3% |

| USD | Retail Sales m/m | 20:30 | 0.4% |

| USD | Empire State Manufacturing Index | 20:30 | -0.9 |

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.