Spreads

Spreads

Spreads

Spreads

Spreads

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.

Stocks experienced a notable upswing on Wednesday as investors found hope in newly released data indicating the Federal Reserve’s potential to manage inflation without triggering a recession in the U.S. economy.

The S&P 500 reached its highest level of the year 2023, reflecting the overall positive sentiment in the market. Bank stocks, including Citigroup and Goldman Sachs, saw significant gains, contributing to the upward momentum.

Although the consumer price index for June rose 3% year-over-year, it fell slightly below economists’ expectations, while the core CPI, which excludes volatile food and energy prices, also rose less than anticipated. While this was viewed as a positive sign, analysts emphasized that the Federal Reserve remains vigilant about areas such as service inflation, wage inflation, and housing inflation, which still persist at uncomfortably high levels.

Investors are closely watching both the consumer price index and the producer price index for insights into future interest rate adjustments by the Federal Reserve. The market currently indicates a strong probability of approximately 92% for a Fed interest rate increase during the July meeting.

As the economy continues to navigate the path of inflation, analysts remain cautiously optimistic, acknowledging that despite positive developments, the Federal Reserve’s decision to cut rates is not yet certain. The market eagerly awaits the release of the upcoming producer price index data for June, which will provide further clarity on inflation trends and potentially impact the central bank’s future moves regarding interest rates.

Data by Bloomberg

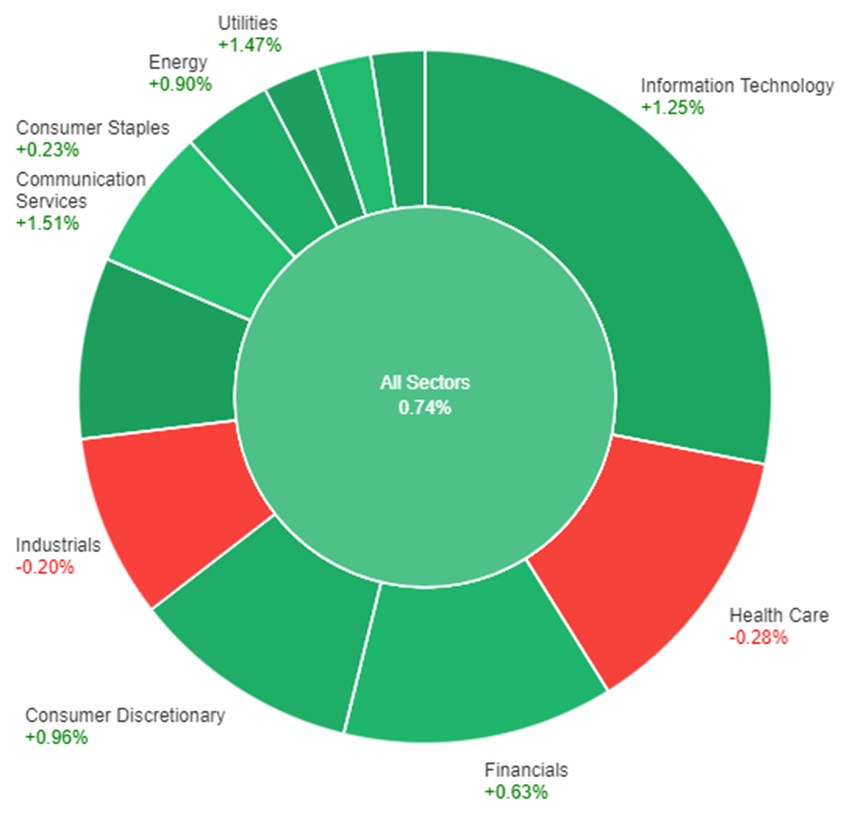

On Wednesday, the stock market showed positive performance across various sectors. The Communication Services sector saw the highest gain, rising by 1.51%, followed closely by Utilities with a 1.47% increase. Materials and Information Technology sectors also performed well, both gaining 1.29% and 1.25% respectively.

Consumer Discretionary and Energy sectors saw moderate gains of 0.96% and 0.90% respectively. Financials and Real Estate sectors experienced smaller increases of 0.63% and 0.44% respectively. Consumer Staples sector had a modest gain of 0.23%. However, Industrials and Health Care sectors faced slight declines, dropping by 0.20% and 0.28% respectively.

On Wednesday, the U.S. dollar index dropped by 1% as the U.S. CPI data came in below expectations. This led to a significant decrease in Treasury yields and pushed the dollar below its prior lows for 2023. Two-year Treasury yields fell by 15 basis points, outpacing the 12 basis point drop in 10-year yields. This shift in yields suggests a potential signal that the Federal Reserve’s hiking cycle may be coming to an end.

The CPI data, along with a relatively positive beige book report, did not change the market’s expectation of a 25 basis point rate hike in July, which has been priced in since the Fed’s pause in June. However, it did reduce the likelihood of further tightening and increased expectations of rate cuts in 2024 by at least 150 basis points.

The euro to U.S. dollar exchange rate (EUR/USD) increased by 1.1% following a breakout above its prior peak for 2023. EUR/USD is approaching its pivotal 200-week moving average at 1.1183, but further disinflationary U.S. data and the Fed’s stance on 2024 rate cuts may impact its future movements.

The U.S. dollar to Japanese yen exchange rate (USD/JPY) fell by 1.47%, trading below June’s low. It briefly dipped below the 38.2% retracement level of its uptrend for 2023. While USD/JPY is oversold on daily studies, there is a possibility of a corrective bounce if it fails to indicate further decline and closes above 138.25.

The significant recovery of the yen could reduce the need for the Bank of Japan (BoJ) to raise its cap on 10-year JGB yields. As a result, pricing by the Fed and Treasury yields remain crucial factors. Sterling (GBP) rose by 0.44%, but its boost was smaller compared to EUR/USD, as it had already broken out above its prior peak for 2023 earlier in the week.

| Currency | Data | Time (GMT + 8) | Forecast |

|---|---|---|---|

| GBP | Gross Domestic Product m/m | 14:00 | -0.3% |

| USD | Unemployment Claims | 20:30 | 251K |

| USD | Producer Price Index m/m | 20:30 | 0.2% |

| USD | Core Producer Price Index m/m | 20:30 | 0.2% |

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.