Spreads

Spreads

Spreads

Spreads

Spreads

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.

Stocks experienced a significant decline on Thursday as the release of stronger-than-anticipated jobs data heightened investors’ apprehension about the state of the economy and the trajectory of interest rates.

The Dow Jones Industrial Average dropped 1.07%, or 366.38 points, closing at 33,922.26, while the S&P 500 and Nasdaq Composite fell by 0.79% and 0.82% respectively. This marked the worst daily performance for both the Dow and S&P 500 since May.

With just Friday’s session remaining in the holiday-shortened trading week, all three major indexes are on track to end the week in negative territory, with the Dow poised for a 1.4% decline, and the S&P 500 and Nasdaq facing losses of 0.9% and 0.8% respectively.

In June, the private sector witnessed a substantial increase of 497,000 jobs, according to data from payroll processing firm ADP, surpassing the Dow Jones consensus estimate of 220,000. This robust gain, the largest since July 2022, exceeded expectations by a wide margin, especially when compared to the downwardly revised 267,000-job addition in May.

The market’s reaction to this positive news indicates that investors may now anticipate a stronger employment report, potentially prompting the Federal Reserve to resume its interest rate hikes after a pause in June.

Traders are pricing in a 92% chance of a rate hike at the central bank’s upcoming meeting, as suggested by CME Group’s FedWatch tool. Amidst these concerns, the Labor Department’s report showing a larger-than-expected decline in job openings in May provides a glimmer of hope that the tight job market could be showing signs of loosening.

Data by Bloomberg

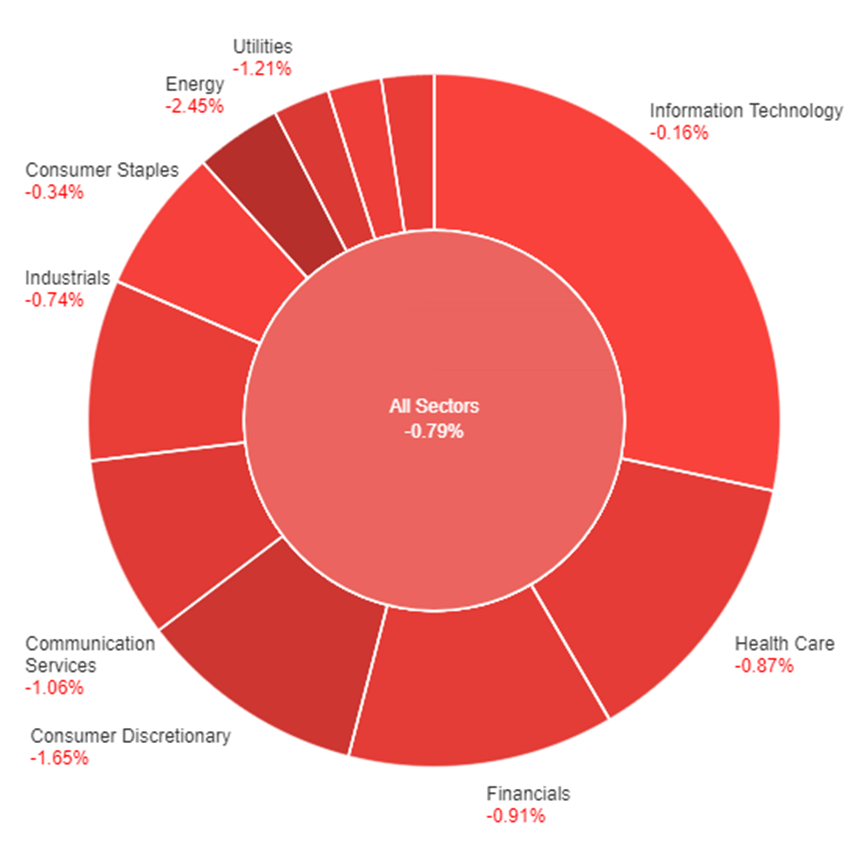

On Thursday, the stock market experienced a broad decline across all sectors, with the S&P 500 index falling by 0.79%. The Information Technology sector showed the smallest decline at 0.16%, followed by Consumer Staples (-0.34%), Real Estate (-0.60%), and Materials (-0.71%).

Industrials and Health Care both dropped by 0.74% and 0.87% respectively. Financials and Communication Services had larger declines at 0.91% and 1.06% respectively, while Utilities experienced a more significant drop of 1.21%.

The Consumer Discretionary sector saw the largest decline of 1.65%. The Energy sector had the most substantial decrease, falling by 2.45% on Thursday. This widespread decline across sectors reflects the overall negative sentiment in the market on that day.

USD/JPY experienced a 0.3% decline following a brief rally, as a combination of risk-off flows and caution ahead of the Non-Farm Payrolls (NFP) report limited gains. The pair struggled to reach the previous day’s high despite a temporary surge in 2-year Treasury yields, which retreated from the 16-year highs seen on Thursday.

The inability to sustain momentum, coupled with speculation surrounding potential Yield Curve Control (YCC) adjustments by the Bank of Japan’s Deputy Governor Uchida, weighed on USD/JPY. Market participants are now eagerly awaiting the NFP report, given the historically weak correlation between the ADP jobs data and the official payroll figures.

Positive outcomes on Friday could reinforce dip-buying strategies, while disappointing data may shift sentiment.

EUR/USD initially pierced the 10-day moving average and reached 1.0901 on EBS during early New York trading. However, the pair reversed course and turned negative as US yields and the US dollar rallied.

The market received a series of indicators pointing to a robust jobs market and a strong economy, subsequently increasing expectations for future Federal Reserve rate hikes, as implied by rates futures. The risk-off sentiment led to a decline in equities and gold prices, while USD/CNH saw gains.

Nevertheless, USD sellers emerged later, pushing EUR/USD into positive territory, hovering near 1.0880 by the end of the session. The formation of a daily doji candle reflects market indecision, with upcoming key data, particularly the US June jobs report and Average Hourly Earnings (AHE), poised to influence further direction. Should the data provide an optimistic outlook, EUR/USD bears may take control.

| Currency | Data | Time (GMT + 8) | Forecast |

|---|---|---|---|

| CAD | Employment Change | 20:30 | 19.8K |

| CAD | Unemployment Rate | 20:30 | 5.3% |

| USD | Average Hourly Earnings | 20:30 | 0.3% |

| USD | Non-Farm Employment Change | 20:30 | 224K |

| USD | Unemployment Rate | 20:30 | 3.6% |

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.