Spreads

Spreads

Spreads

Spreads

Spreads

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.

On Wednesday, the Dow Jones Industrial Average experienced a decline as Wall Street returned from the Fourth of July holiday break. Investors analyzed the recently released minutes from the Federal Reserve meeting, seeking insights into the current state of monetary policy.

The Dow dropped by 129.83 points or 0.38%, closing at 34,288.64, while the S&P 500 fell 0.2% to 4,446.82, and the Nasdaq Composite slipped 0.18% to end at 13,791.65. This marked the end of three-day winning streaks for both the Dow and S&P 500.

The minutes revealed that most officials indicated the possibility of future interest rate hikes, which made investors more cautious due to concerns about the market and economic trajectory for the second half of the year.

The released data on Wednesday morning showed weaker-than-expected factory orders in May, further contributing to market uncertainties. Investors will be closely monitoring employment and wage data later in the week to gauge the strength of the labour market.

The previous week had been positive for the Nasdaq, which had its best first half of the year since 1983, and the S&P 500, which saw its best first-half advance since 2019. However, the Dow had a more modest gain of only 3.8% during the same period.

The holiday-shortened week brought attention to the impact of the Federal Reserve’s rate hike policies on market sentiment and expectations for the rest of the year.

Data by Bloomberg

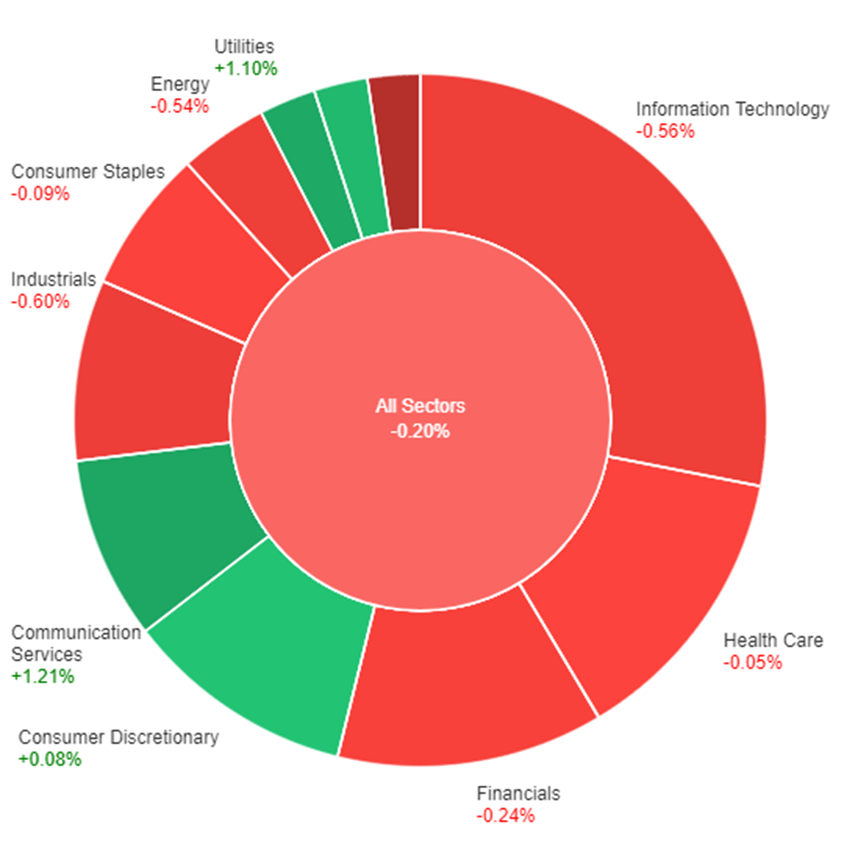

On Wednesday, the overall performance of the stock market saw a slight decline of 0.20%. However, some sectors managed to buck the trend and achieve positive gains. Communication Services experienced the highest increase of 1.21%, followed closely by Utilities with a rise of 1.10%.

Real Estate also showed a modest growth of 0.47%. On the other hand, certain sectors faced losses, with Materials taking the biggest hit at -2.47%. Energy and Information Technology also saw declines of -0.54% and -0.56% respectively.

The remaining sectors, including Consumer Discretionary, Health Care, Consumer Staples, Financials, Industrials, and Materials, all experienced smaller drops ranging from -0.05% to -0.60%.

In Wednesday’s trading, the dollar index experienced a 0.3% gain, seen as a precursor to important upcoming data releases in the United States on Thursday and Friday. The dollar’s performance was supported by weaker-than-expected data and risk-off sentiment due to concerns in the market.

The Federal Reserve’s minutes from their recent meeting confirmed existing expectations of a hawkish stance. The decision by the Reserve Bank of Australia to keep interest rates unchanged on Tuesday also contributed to the dollar’s strength.

Additionally, with major central banks raising rates to combat inflation and uncertainties surrounding China’s economy, investors turned to the dollar as a safe haven. As a result, the AUD/USD pair fell by 0.54%, while the USD/CNH pair surged by 0.42%.

The focus in the coming days will be on the release of key US reports on Thursday, including data on layoffs, jobless claims, ISM services, and JOLTS. This will be followed by Friday’s highly anticipated payroll report.

These upcoming reports overshadowed the impact of the Federal Reserve’s minutes, particularly after a series of comments made by policymakers indicating the possibility of two more interest rate hikes this year.

While forecasts suggest a slightly less hawkish stance from the Fed compared to previous periods, it is worth noting that non-farm payrolls have consistently exceeded expectations this year. Investors will be closely watching the expected figure of 225,000 jobs added in June, following the substantial increase of 339,000 in May.

If this week’s data continues to present conflicting signals, as some recent releases have, then the significance of Wednesday’s consumer price index (CPI) will grow. Expectations for Fed rate hikes have remained relatively stable, with a skipped hike in June and a projected 25 basis point increase in July or, at the latest, September.

There is only about a 35% probability of a final rate increase beyond that. The euro fell by 0.25%, briefly touching the daily cloud support level that held June’s lows at 1.08355 on EBS. The European Central Bank is expected to raise rates by 25 basis points two more times.

The Japanese yen, on the other hand, rose by 0.14% after a temporary drop towards 144, a level where 2.38 billion of options are set to expire on Thursday. The yen’s upward trend is consolidating within a range of 144-145 as currency traders await key US data releases.

The British pound declined by 0.16% as investors weigh the potential economic consequences against the market’s pricing of 143 basis points of Bank of England rate hikes.

Economic Data

| Currency | Data | Time (GMT + 8) | Forecast |

|---|---|---|---|

| USD | ADP Non-Farm Employment Change | 20:15 | 226K |

| USD | Unemployment Claims | 20:30 | 247K |

| USD | ISM Services PMI | 22:00 | 51.3 |

| USD | JOLTS Job Openings | 22:00 | 9.93M |

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.