Spreads

Spreads

Spreads

Spreads

Spreads

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.

In a temporary halt to the recent market rally, stocks experienced a decline on Wednesday. Investor sentiment was influenced by Federal Reserve Chair Jerome Powell’s remarks on inflation. The Dow Jones Industrial Average dropped 0.30%, the S&P 500 declined by 0.52%, and the Nasdaq Composite slid 1.21%, marking the third consecutive day of losses for all three indexes.

The pullback was particularly evident among major tech stocks that had seen significant gains due to the hype around artificial intelligence. Amazon shares fell by approximately 0.8% following a lawsuit by the Federal Trade Commission, accusing the company of misleading customers and obstructing cancellation attempts. Nvidia, which witnessed an impressive 200% surge this year, saw a 1.7% decrease. Google-parent Alphabet and Netflix also experienced declines of over 2%.

The decline in stocks was further fueled by disappointing earnings reports. FedEx shares fell over 2% after reporting weaker-than-expected revenue for the last quarter, while Winnebago’s shares dropped nearly 1.3% due to the company’s failure to meet third-quarter revenue estimates.

Investor attention was also drawn to Powell’s statements, where he indicated the likelihood of future interest rate hikes in response to combating inflation. Although the central bank refrained from raising rates after 10 consecutive hikes, Powell mentioned the possibility of two more quarter-percentage-point moves this year.

This cautious outlook contributed to the pause in the recent market exuberance, as investors reassessed their positions following the S&P 500’s highest level since April 2022 and its five consecutive positive weeks.

Data by Bloomberg

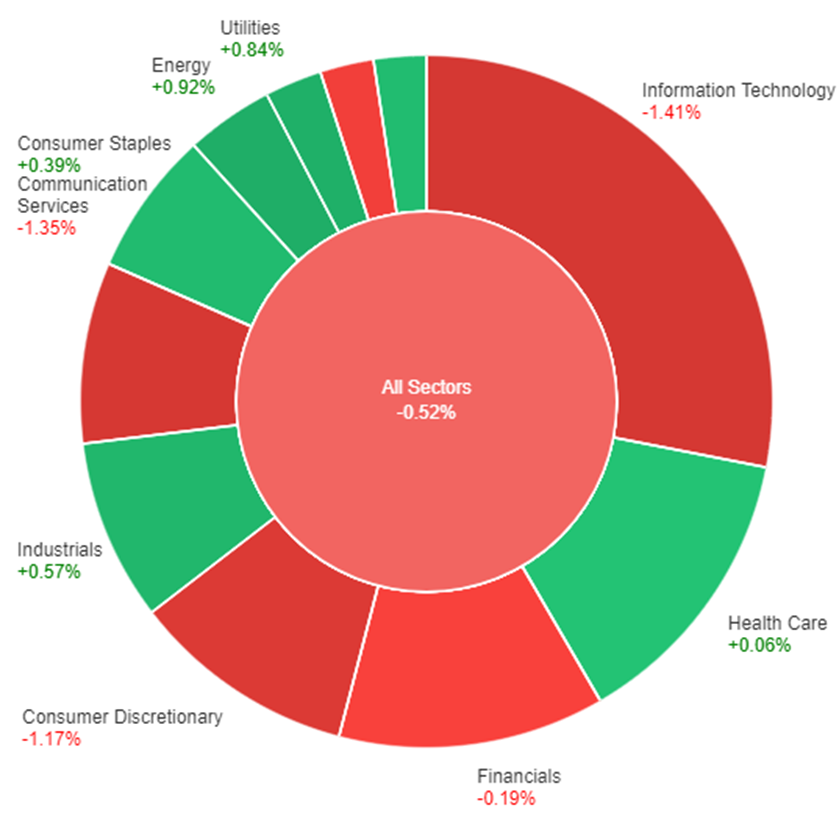

On Wednesday, there were varied price changes across different sectors. The energy sector experienced a positive gain of 0.92%, followed by utilities with a gain of 0.84%, and industrials with a gain of 0.57%. Consumer staples and materials sectors also saw modest gains of 0.39% and 0.35% respectively. Health care had a minimal increase of 0.06%.

However, some sectors experienced losses. The largest decline was observed in the information technology sector, which had a decrease of 1.41%. This was followed by communication services with a decline of 1.35%, and consumer discretionary with a decline of 1.17%. The financials sector also experienced a slight decrease of 0.19%. Real estate had the largest loss among the sectors, with a decline of 0.45%.

On Wednesday, the dollar index experienced a 0.45% decline as Fed Chair Jerome Powell’s testimony and comments indicated uncertainty about the extent of future policy tightening by the U.S. central bank. Powell’s comparison of the gradual tightening to slowing down a car as it approaches its destination worried dollar traders, leading to further losses.

Meanwhile, EUR/USD rose by 0.65%, surpassing previous highs after the Fed and ECB meetings, and approaching the significant psychological barrier of 1.10. The market expects two more rate hikes from the ECB before a prolonged plateau, while only one additional hike from the Fed is anticipated before rate cuts begin next year.

Sterling initially experienced losses but later recovered, returning to a flat position. Concerns about the UK’s inflation, which reached its highest level since 1992 at 7.1% in April, raised worries that the Bank of England (BoE) would need to implement substantial tightening measures, potentially leading to a challenging economic situation.

Market uncertainty regarding the extent of rate hikes by the BoE resulted in a 10-basis point increase in two-year gilts yields. However, expectations remain steady at a total of 150 basis points of hikes and a terminal rate of 6%. The doubts surrounding additional Fed hikes pulled the sterling up from its 10-day moving average support level of 1.2691, edging closer to Tuesday’s highs.

On the other hand, the Bank of Japan (BoJ) maintained its negative policy rate, implemented yield curve control, and engaged in extensive asset purchases. This policy contrast with other central banks, including the Fed, propelled USD/JPY to new highs in 2023 at 142.37.

However, significant resistance at 142.50 prevented further gains. To surpass this resistance, USD/JPY may require support from U.S. jobless claims data on Thursday and Japan’s consumer price index (CPI) release on Friday, reinforcing the bullish divergence between the Fed and BoJ policies.

| Currency | Data | Time (GMT + 8) | Forecast |

|---|---|---|---|

| CHF | SNB Monetary Policy Assessment | 15:30 | |

| CHF | SNB Policy Rate | 15:30 | 1.75% |

| CHF | SNB Press Conference | 15:30 | |

| GBP | MPC Official Bank Rate Votes | 19:00 | 7–0–2 |

| GBP | Monetary Policy Summary | 19:00 | |

| GBP | Official Bank Rate | 19:00 | 4.75% |

| USD | Unemployment Claims | 20:30 | 261K |

| USD | Fed Chair Powell Testifies | 22:00 |

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.