Spreads

Spreads

Spreads

Spreads

Spreads

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.

Stocks experienced a decline on Tuesday, marking the first trading day of the week, as the market took a breather after a recent rally that had propelled it to levels not seen in over a year. The Dow Jones Industrial Average fell by 245.25 points (0.72%) to reach 34,053.87, while the S&P 500 and Nasdaq Composite declined by 0.47% and 0.16%, respectively. Energy stocks, along with Intel, Nike, and Boeing, weighed on the market with notable drops of more than 3%. Conversely, homebuilders, including PulteGroup, D.R. Horton, and Lennar, outperformed following a robust housing report. Nvidia also defied the downward trend, posting a gain of over 2% amidst the broader market decline.

Investors were coming off a strong week, with the S&P 500 and Nasdaq Composite delivering their best weekly performances since March. The S&P 500 rose 2.6% and the Nasdaq gained 3.25%, while both indexes reached their highest levels since April 2022. The market responded favorably to the Federal Reserve’s decision to skip a rate hike in June, although policymakers are projecting two quarter-point increases later in the year. Despite uncertainties surrounding future Fed policies, investor bullishness has been on the rise, reaching its highest level since November 2021. As economic data remains limited in the current shortened trading week, traders are closely monitoring market sentiment and its potential impact on stock performance.

Data by Bloomberg

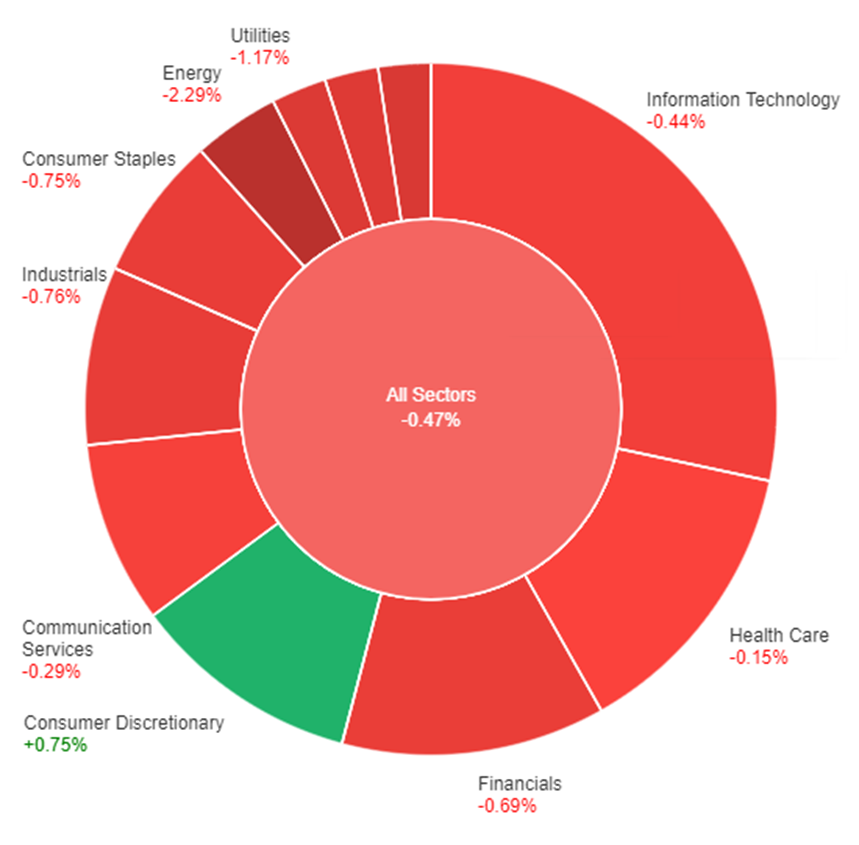

On Tuesday, the overall market performance showed a decline of 0.47% across all sectors. However, there were a few sectors that experienced positive movement. Consumer Discretionary had a gain of 0.75%, indicating increased consumer spending on non-essential goods. In contrast, Health Care saw a slight decrease of 0.15%. Communication Services and Information Technology both experienced declines of 0.29% and 0.44% respectively. Financials had a larger decline of 0.69%, while Consumer Staples and Industrials experienced decreases of 0.75% and 0.76% respectively. Real Estate and Utilities were among the sectors with the largest declines, with decreases of 1.11% and 1.17% respectively. Materials and Energy had the most significant declines, with decreases of 1.26% and 2.29% respectively, indicating a negative trend in these sectors.

Last week, the US dollar and Japanese yen experienced declines against major currencies, which were corrected this week. The correction came ahead of Federal Reserve Chair Jerome Powell’s upcoming testimony and was driven by factors such as the Fed’s pause in rate hikes, the ECB’s ongoing rate hiking efforts, and the Bank of Japan’s commitment to maintaining its easing policies. The euro faced pressure due to a drop in German PPI and the euro zone’s current account surplus. Additionally, the market responded to a significant increase in US housing starts. Meanwhile, the UK pound fell after a sharp surge, and the yen strengthened against the Australian dollar, pound, and euro, influenced by Treasury yields and safe-haven demand.

This week, all eyes are on Powell’s testimony as the market seeks clarity on the Fed’s future monetary policy direction. Market expectations currently suggest only one more rate hike, contrasting with the Fed’s projection of two additional hikes. Meanwhile, the euro is anticipated to see a slower retreat compared to the US dollar, with the market pricing in two more rate hikes by the ECB. In the UK, there is anticipation around the BoE meeting and the possibility of a rate hike. The market currently prices in a 25 basis point hike, with a chance of a 50 basis point hike. Overall, market dynamics and central bank actions continue to shape currency movements, with investors closely monitoring economic indicators and policy announcements.

| Currency | Data | Time (GMT + 8) | Forecast |

|---|---|---|---|

| GBP | Consumer Price Index | 14:00 | 8.4% |

| USD | Fed Chair Powell Testifies | 22:00 |

Make informed decisions with the most up-to-date and reliable financial data, exclusively provided by vtmarkets.com.